James Childress confirms movement of money between funds and ongoing general fund deficit, offers recommendations to Saratoga Town Council

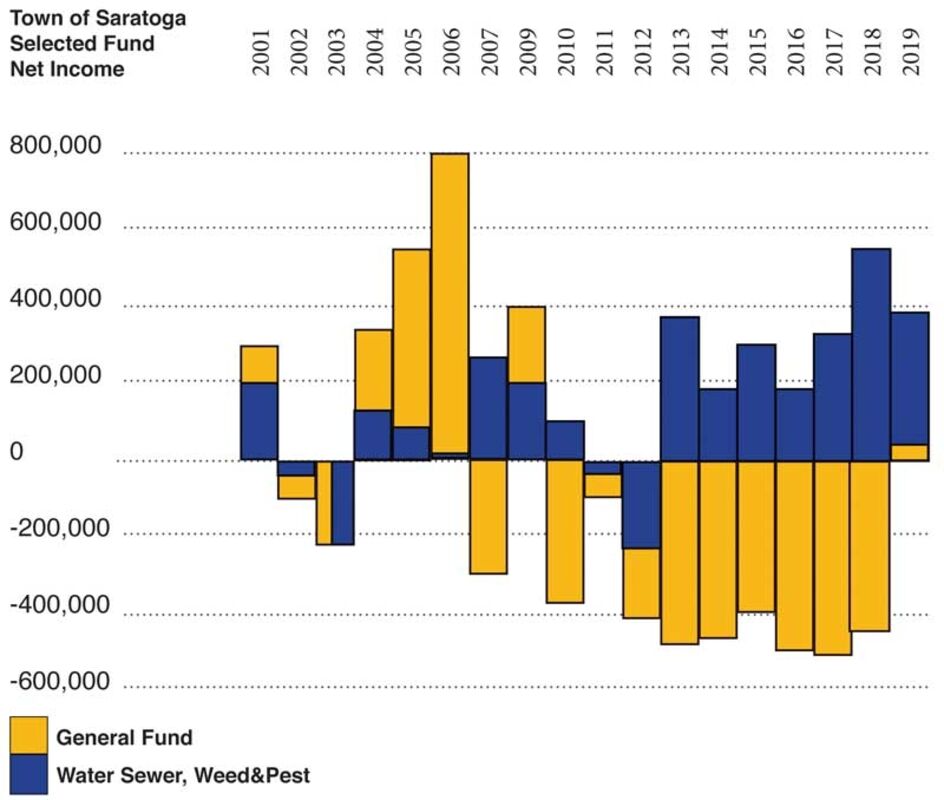

"You're going to see, 2010 through 2018, that whole time we're below the bar. That ends up being $3.7 million in total losses through that period of time. So, again, the town's in a pickle."

Five weeks after his last appearance before the Saratoga Town Council, James Childress of Childress Accounting and Consulting appeared before the governing body on June 23 to provide sobering news. Not only did the general fund see a deficit of $3.7 million over eight years, but Childress and his team went back 20 years to find a "neutral point" that would not skew their numbers.

Preparing a Number

While it had been known there was activity between the general fund and the enterprise funds following a February 28 email from Childress to the Town of Saratoga (see "Casting a dissenting vote" on page 1 of the March 11 Saratoga Sun), the exact level of activity had been unclear. During a March 11 workshop between the Town of Saratoga, Childress and auditors Carver, Florek and James (CFJ), the desire for interfund payables and receivables-also called a due to/due from-to be recorded had been expressed.

"In an accrual basis financial statement, you would have this interfund payable in one fund and an interfund receivable in another fund," said Childress on June 23. "However, in the case of the town, you're cash basis; 100 percent cash basis. So, you show cash and fund balance. You have no place to put an interfund payable or receivable. It doesn't fit in your financial statement set."

Childress added that the Town of Saratoga had been recording interfund transfers-which varies from an interfund payable and receivable in that a transfer is a one-way movement of money-for "quite a long time."

"They should always be done on purpose; they should always be thought out; they should include considerations about whether funds are restricted, designated, reserved, whether they are truly free and able to move from one fund to another," Childress said.

According to Childress, because the town has operated entirely on a cash basis of accounting, there was no place to put an interfund payable and receivable and so was recorded as an interfund transfer. The Town of Saratoga's accounting system operates on pooled cash, meaning that all funds share a bank account but are supposed to be separated in the town's system.

Childress further stated that working to include interfund payables and receivables, which is found in accrual basis accounting, provided some difficulty due to the town's reliance on cash basis accounting. He added that those disclosures in the statement set were not uncommon, as larger entities such as the City of Cheyenne and the State of Wyoming would often show them.

"In your case, you've never had to evaluate these numbers and you don't actually, in your accounting system, have a historical record of these transactions," said Childress. "It just doesn't exist."

The introduction of interfund payables and receivables led to the introduction of another accrual basis accounting concept; interfund overhead allocations. As was reported previously (see "What is a reasonable allocation" on page 1 of the May 27 Saratoga Sun), the introduction of these allocations was contested by Councilmember Jon Nelson.

"In this case, we have to prepare a number. We've been asked to do that and so there's all of these things that are considerations that we can't exclude, we can't pick and choose," Childress said. "In this case, interfund overhead is something that we would consider to be fair across all funds."

Later, as he fielded questions from the public and the council, Childress stated that $30,390 would be the balance of the general fund effective June 30, 2019 with an interfund payable to the enterprise funds in the amount of $1,037,000.

Tighten it Up

Childress said he applauded the Saratoga Town Council's efforts to determine the numbers in terms of interfund payables, receivables and transfers.

"But it's also true that this is now considered an item that's materially important to your audit and your audit needs to get done," said Childress. "Which means, if we got to make it tight and keep it together with a little bit of bubblegum, for now, that's appropriate. We just wanted to get to a point where you could button this up, maybe some duct tape if we had to, and get to a point where you could say, 'This is a starting point. We can move forward from here.'"

Throughout the presentation, Childress stressed that the amounts reached following the 20 year study were estimates.

"It's an estimate and it will remain an estimate, I think, until you approach some of these outside parties like the (Saratoga-Carbon County) Impact Joint Powers Board ... and you say, 'Hey, we think we have an issue here' because you do," Childress said. "You have an amount of money that's been pulled from those funds. The money went out. It went out of the general fund and just by the basic action of cash-we can't have a negative-it also went out of these other funds."

Action of cash was a term used by Childress multiple times throughout the presentation, in which he stated that the Town was forced to make decisions about transfers from other funds. According to Childress, because the Town of Saratoga cannot statutorily show a negative fund balance, the "action of cash" resulted in money being moved from one fund to another.

"(There's) nothing else that moves and shakes in your financial statement except for cash to show either zero or positive, but you can't have a deficit fund balance," said Childress. "You have to manage to avoid that."

Money Moving

While Childress acknowledged that, for a consistent period of eight years, the general fund had been in deficit he also stated that there had been times in that 20 year period in which the general fund had "bailed out" other funds with its surplus. Again using the term "action of cash", Childress said "the money has to come from somewhere."

He added that as his team considered where the funds could have been transferred from, they ruled out the airport fund due to federal grant compliance and special revenue funds, such as the Specific Purpose One Percent Sales and Use Tax (6th penny tax), as they were intended for a specific project.

"There's only one other place it could have come from. It has to come from somewhere; water, sewer, weed and pest. Enterprise funds," said Childress. "It's not the best news of the day but that's the box we find ourselves in."

According to Schedule C of the report presented to the Town of Saratoga, which included fund balances and estimated interfund overhead for the 20 year period ending June 30, 2019, a total of $1,075,277 was listed as an interfund payable. That total number broke down to $951,384 from the water fund, $37,618 from the sewer fund and $86,274 from the weed and pest fund.

Allocating the Basket

Under discussion of the interfund overhead allocation, Childress informed the Saratoga Town Council that he and his team had examined over 100,000 transactions in the 20 year period to determine which could be considered an overhead allocation and which were clearly an interfund payable and receivable.

In his report, he listed certain expenditures as being able to contribute to a basket for use in an allocation of interfund overhead. Those expenditures included; salaries, health insurance, travel, supplies, advertising, utilities, bank charges, contract services, communications, payroll benefits, pension fund, training, insurance, repairs, telephone, professional fees and membership dues.

"The objective of this development of the 'basket' was to provide a fair application of the overhead while not going into a level of detail that would be cost prohibitive," wrote Childress in the report. "In future periods, the Town may consider using employee time sheets, or equipment logs, to assist in this process."

The report also read that the general fund owes a debt to the water, sewer, and weed and pest funds ranging from $737,000 to $1.1 million.

"This bears the caveat that the historical net transfer deficit may indeed be properly recorded among the water, sewer, and weed and pest funds rather than the general fund," Childress wrote. "Were that the case, this amount would be reduced to $737,000."

When questions were asked about the overhead allocation, it was asked by SCCIJPB Chairman Richard Raymer if Childress had considered the $12,000 annual payment made to the Town of Saratoga for administration costs. Childress stated that he was not aware of that payment.

"I'm an outside party and so I'm looking at all of these transactions," said Childress. "Every single one of these could have a hair sticking out that needs to get caught and combed down."

Recommendations

After going over his report with the Saratoga Town Council, Childress provided a number of recommendations to the governing body. The most important was that the Town of Saratoga needed to sign the representation letter from CFJ and complete their audit.

"Let yourself be kind of guided by the fact that you have an estimate," said Childress. "You have a disclosure related to an estimate and that's a very important thing for you to say, 'Okay, this doesn't need to be perfect. We're not subject to that burden of proof in this audit.' It's essential that you get your audit done. It's absolutely essential."

The other recommendation was that the governing body would need to closely monitor their combined, or pooled, cash if they continued with the cash basis accounting. If the Town of Saratoga found that to be too difficult, Childress said, they would need to move away from the pooled cash system and assign individual bank accounts for each entity, such as the water, sewer, and weed and pest funds.

"Those are basically your two options there," Childress said.

After nearly two and a half hours of discussion and questions, the governing body voted 3-1 to accept Childress' report with Nelson voting against.

In the days after the June 23 meeting, emails between members of the council and to members of the media began discussing the scheduling of a workshop to discuss the recommendations from Childress. As of press time, a date has not been set.

The next meeting of the Saratoga Town Council will be at 6 p.m. on July 7 at Saratoga Town Hall.

Reader Comments(0)